The application underlying this decision relates to managing the funding of catastrophe relief efforts. However, the European Patent Office refused to grant a patent that mainly focuses on a payment method. Here are the practical takeaways of the decision T 0550/14 (Catastrophe relief/SWISS RE) of September 14, 2021 of Technical Board of Appeal 3.5.01:

Key takeaways

The invention

The Board in charge summarized the invention as follows:

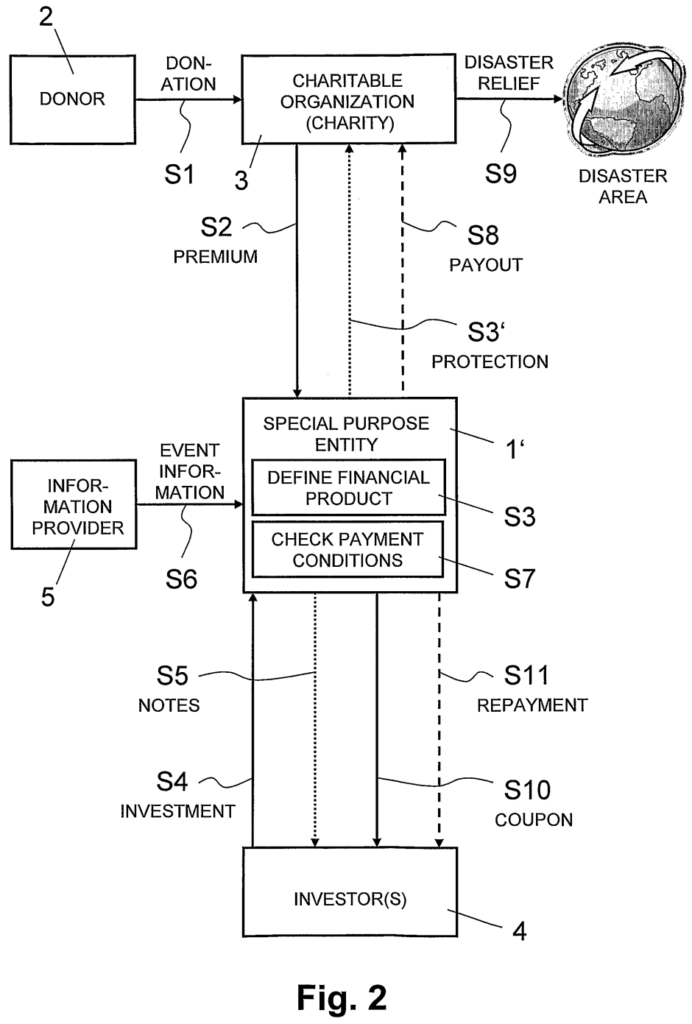

1.1 The invention is about managing the funding of catastrophe relief efforts caused by natural or man-made disasters, such as earthquakes, see page 1, first paragraph of the originally filed application. Conventionally, as can been from Fig. 2, charitable organisations 3 provide relief S9 in the event of a disaster from donations S1 from donors 2. Insurance companies might offer catastrophe insurance policies, but these may be too expensive or even unavailable for developing countries, so that the available relief may be insufficient.

1.2 The objective of the invention is to make sure that adequate funding is in place before the catastrophic event actually occurs and to pay out when it does.

1.3 The invention achieves this by providing a “special purpose entity” (“special purpose vehicle” in the claims) 1′ which offers a financial product S3 (e.g. a security, or another financial instrument) in return for a premium S2 from the charitable organisation (or donor directly), see page 2, last paragraph, to page 3, first paragraph.

1.4 Investors 4 back S4 the product and receive in return for their investment a payment of the premium S2 which is issued as a coupon S10 from the special purpose entity. If a catastrophic event occurs within a defined time period, the capital is paid S8 to the charitable organisation, otherwise the capital is paid back S11 to the investors who keep the premium for their efforts.

1.5 The “special purpose entity” collects information S6 about catastrophic events from an online provider 5, see page 7, lines 8 to 16. This information is provided in the form of a “parametric index” indicating the severity of catastrophic events, which serves as a triggering condition for whether and how much payout shall be made to the charitable organisation, see page 10, third paragraph. The “parametric index” is linked to geographical areas, the type of catastrophe and the severity of the catastrophic event (Table 1).

Fig. 2 of WO 2009/100546 A1

Here is how the invention is defined in claim 1 of the main request:

-

Claim 1 (Main Request)

Is it technical?

According to the assessment of the Board in charge, the closest prior art for the claimed subject-matter is a common computer network and that claim 1 differs from such a network by all features relating to the claimed payout scheme:

2.7 The Board agrees with the division that a valid starting point is a networked computer system, comprising a control module and several functional modules. Such a “networked” system can be interconnected with other networked computers via a telecommunications network and not just be a stand-alone system, as argued by the appellant.

2.8 The invention therefore differs, as is usually the case starting from such prior art, by all the features of the relief payout scheme.

Then, the Board assessed whether the first instance examining division was correct in considering all the distinguishing features non-technical. As a result, the Board held the the examining division’s assessment was correct:

2.10 The Board agrees with the division that the features define a method for managing funding of catastrophe relief efforts. They represent the different parties involved, which are the donor, the charitable organisation, the investor and the information provider, as well as the monetary and information flow between them and the role each one plays. They are therefore part of the business requirements given to the skilled person to implement.

Contrary to the opinion of the Appellant, the Board also considered the claimed parametric trigger as non-technical:

2.11 … For instance, a catastrophe of a hurricane in the Caribbean, as shown in Table 1 on page 7, has the parametric trigger of wind speed, size of storm and location. In the Board’s view, determining this parametric information, the triggering criteria and the trigger level does not require any technical considerations. Furthermore, the business person would be aware that the relevant information would be available from providers for weather data and catastrophe information.

2.12 2.12 The Board therefore sees no need for the business person to have technical knowledge about networked computer systems in order to propose the business method of the invention. …

Finally, the Board held that implementing a business scheme as claimed would not pose any difficulties to the skilled person:

2.13 Finally, the Board cannot see any difficulties for the person skilled in the art of data processing to implement the business concept of the present invention on the networked computer system.

The Appellant did not agree and requested remitting the case back to the first instance to further discuss technicality of, for example, the parametric trigger as mentioned above:

3.1 … Moreover, if there were no arguments why certain features were deemed to be part of the business model, the right to be heard was not respected. In the present case, a more detailed discussion should have taken place about the feature “parametric trigger”, …

However, the Board held that in the present case it is clear that the features in questions are non-technical. Moreover, the Board considered that these features have already been sufficiently discussed in the first instance proceedings:

3.2 The Board agrees that in this field there is a danger of simply asserting that certain features are non-technical with no basis. Indeed, the Board has seen decisions where the reasoning has not been fully convincing. But this is not one of them. As mentioned above, the examining division addressed the argument about the parametric trigger in the decision at points 2.3 and 2.3.1. Furthermore, the division admirably minuted the discussion of this point at page 2, third last paragraph. This shows why it is always advisable to minute clearly the arguments exchanged about contentious points.

As a result, since non-technical features have to be ignored for assessing non-obviousness, the Board dismissed the appeal due to lack of inventive step.

More information

You can read the whole decision here: T 0550/14 (Catastrophe relief/SWISS RE) of September 14, 2021