This decision concerns an invention related to automated payment upon sensing departure from a location. Applying the COMVIK approach, the Board noted that since automatic charging is part of the non-technical business aim to be implemented by the skilled person, and has no significance for the purpose of assessing inventive step and any analysis of the benefits or drawbacks of automatic charging is irrelevant. The Board noted that the business person is always looking to reduce resource requirements, and will envisaging a single payment arrangement which would automatically charge the customer at the end of their visit to the outlet. Since the implementing automatic charging would be within the capabilities of a skilled programmer, it is obvious. Here are the practical takeaways from the decision T 0351/19 of June 23, 2022, of the Technical Board of Appeal 3.4.03.

Key takeaways

The invention

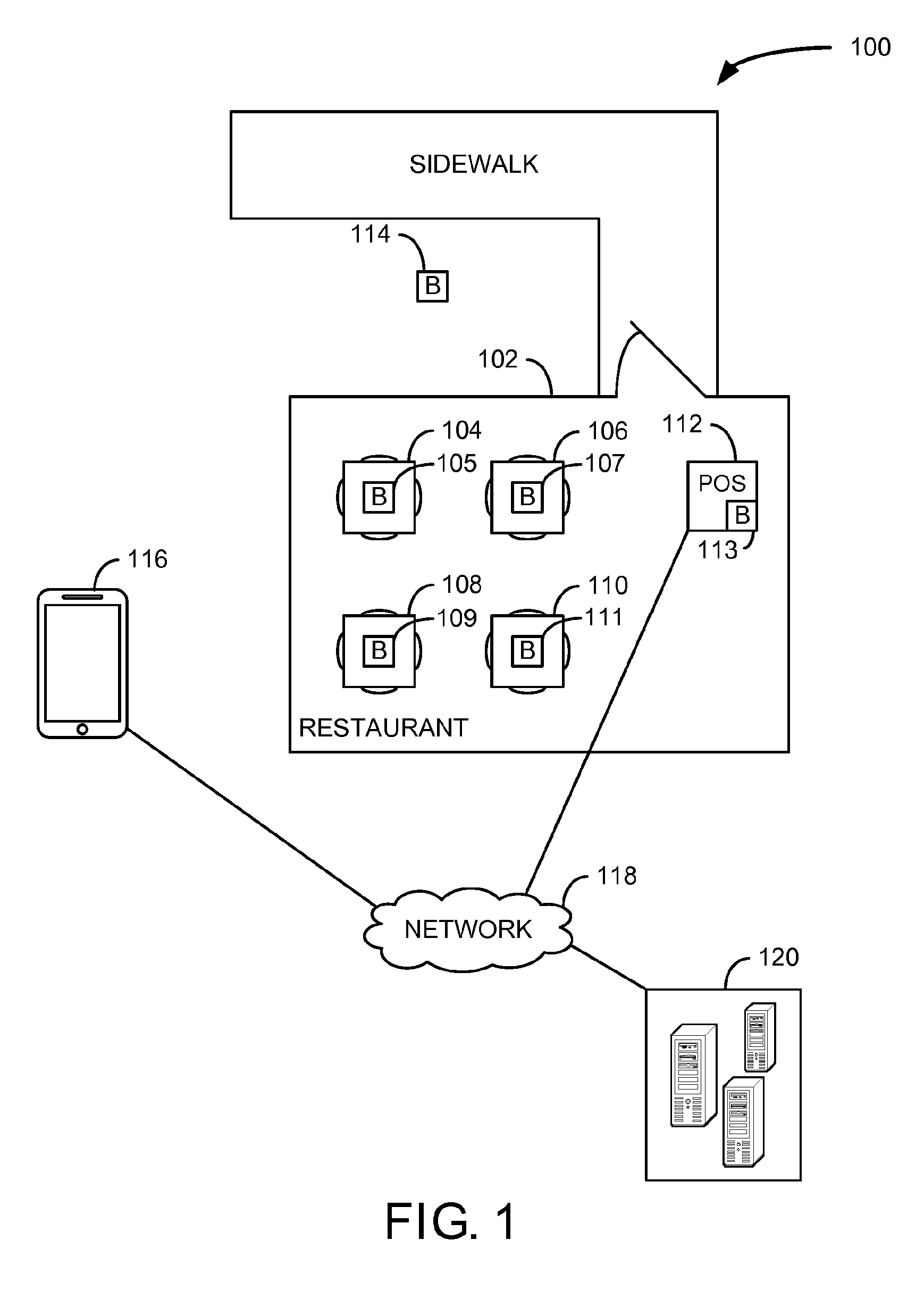

At retail outlets, customers often wait in lines to pay for items and services. This is true even at restaurants where there may be a line at a point of sale terminal or simply for wait staff to return with a check and then to return with proper change or a bank card used to pay.

The invention aims to be implemented at retail outlets (e.g., restaurants, salons, stores, etc.) to automatically charge a customer account for ordered items upon an automated detection of a customer retail outlet departure.

This is achieved by having the customer account at the retail store linked to a mobile device, determining if the device has departed from the retail outlet, and automatically charging the amount payable to the account linked with the customer.

-

Claim 1 of the Main Request

Is it patentable?

In the first instance, the Examining Division refused the application on the grounds that the claimed subject-matter did not involve an inventive step within the meaning of Article 56 EPC. The applicant argued that the

The Board first identified the non-technical features of the claimed invention to apply the COMVIK approach:

3.1 In a retail outlet, the location at which a customer is expected to pay for goods or services (for example, at a table, at a bar or counter, or at the exit) is a decision relating to the administration of the outlet, to be taken by a business person in the light of business or commercial considerations. The same is true of how often payment is to be made (for each separate purchase or only once with a final bill), and the types of payment which are accepted.

3.2 In the present case, payment being made upon departure from a retail outlet, charging being automatic, i.e. without requiring customer intervention, and charging a specific amount to a customer payment account are all business considerations. The following features of claim 1 are therefore seen as non-technical features:

– “has departed a retail outlet”;

– “automatically charging the amount payable to a payment account associated with the customer account”; and

– “the automatic charging including … payment account data and the amount to be charged”.

3.3 Since the claim comprises both technical and non-technical features, the Board makes use of the well-established “Comvik” approach set out in T 641/00 (see Case Law of the Boards of Appeal of the European Patent Office, 9th edition 2019, I.D.9.1.3 b)). The appellant also stated at oral proceedings that it was arguing in line with Comvik.

According to this approach, “where a feature cannot be considered as contributing to the solution of any technical problem by providing a technical effect it has no significance for the purpose of assessing inventive step” (T 641/00, Reasons, point 6, first paragraph). However, “where the claim refers to an aim to be achieved in a non-technical field, this aim may legitimately appear in the formulation of the problem as part of the framework of the technical problem that is to be solved, in particular as a constraint that has to be met” (T 641/00, Reasons, point 7, second paragraph).

The Board then identified the distinguishing features over the closest prior art to identify the technical problem:

3.4 The Board sees paragraphs [0066] and [0067] of D1 as a suitable starting point for the inventive step analysis, and the appellant has not disputed that the following features are disclosed in these paragraphs: “A method (200) comprising:receiving, via a network (118) from a mobile device (116) associated with a customer account, first data indicating the mobile device (116) has departed a retail outlet (step 208)”.

3.5 The appellant argues that the remaining features of claim 1 are not disclosed in D1, hence the features distinguishing the claimed subject-matter from D1, are as follows: “and upon receiving the first data;generating, from stored retail session data, a final bill including an amount payable (step 210); andautomatically charging the amount payable to a payment account associated with the customer account (step 212), the automatic charging including transmitting payment account data and the amount to be charged to a transaction processing system”. The appellant argues that “and upon receiving the first data” applies to all of the subsequent steps (“generating”, “automatically charging” and “transmitting”), and while some elements of the above features might be disclosed per se in D1, they are not disclosed as being carried out “upon receiving the first data” or at the departure of the customer from the retail outlet, as in claim 1. The Board sees no reason to depart from this analysis.

3.6 In the present case, in the light of the non-technical features identified above under point 3.2, the essential business aim of the invention is ensuring that the customer is automatically charged the final amount when they leave the outlet, and according to the Comvik approach, this business aim may appear in the formulation of the objective technical problem. The Board therefore regards the objective technical problem as being to implement the automatic charging of the final amount to the customer when they leave the outlet. It is to be understood that this represents a concise formulation of the problem to be solved, and that the problem actually encompasses the technical implementation of all of the features listed above as non-technical under point 3.2, including, for example, “automatically charging the amount payable to a payment account associated with the customer account”.

The Board finds it plausible that those distinguishing features of claim 1 which have a technical character represent a solution to this problem, at least at a very high level.

3.7 In the letter dated 28 April 2022, page 3, first paragraph, the appellant proposed that the problem might be seen as “how to implement automatic payment as the customer leaves the retail outlet to avoid the customer being required to wait in a queue to pay”, which the Board sees as essentially the same as its own formulation of the problem, as stated above under point 3.6. At oral proceedings, the appellant proposed a slightly different version of the problem, namely how to implement the automatic transaction payment to avoid the user having to wait for the manual transaction to be effected. This formulation is unsatisfactory, as it fails to take into account one of the non-technical aims of the invention, namely that the automatic payment is to be carried out upon the customer departing the retail outlet.

Once the technical problem (which included the non-technical aim of the invention) was formulated, the Board noted that the technical implementation was obvious to the skilled person:

3.8 As noted above under point 3.4, the appellant has not disputed that D1, in paragraph [0066], discloses a method for determining whether the customer has departed the outlet corresponding to that set out in claim 1 of the main request. A solution to the present objective problem would require inter alia the implementation of a method for determining whether the customer had departed the outlet, and it would be obvious for the skilled person to adopt the method disclosed in D1 in seeking a such a solution.

3.9 A solution of the objective problem would also require the skilled person to implement automatic payment upon the determination that the customer had left the outlet. Payment using a mobile device was well-known at the priority date of the present application (see e.g. D1, paragraph [0004]). Moreover, it would be obvious to the skilled person starting from paragraph [0066] of D1 to look to the remainder of that document, which discloses numerous examples of payment methods using mobile or wireless devices. Hence, no inventive step can be seen in effecting payment using the customer’s mobile device.

3.10 According to D1, the wireless device may be set up to place an order, request a service etc. (paragraph [0023]), hence, in the terminology of claim 1 of the present application, “retail session data” would be stored. Any electronic payment method necessarily involves a determination of the amount to be paid, and therefore generating a final bill on the basis of what has been purchased (“retail session data”) including an amount payable would be obvious. Charging the amount payable for a purchase to a customer’s payment account is a business feature which is commonplace in electronic commerce (see e.g. D1, paragraph [0045]), the implementation of which would be obvious to a skilled programmer. Similarly, transmitting payment account data and the amount to be charged to a transaction processing system is commonplace in electronic commerce (see e.g. D1, paragraph [0045]), and implementing such a step would present no difficulty to the skilled programmer.

In short, implementing the business aims of the present invention in the manner claimed would be obvious to the person skilled in the art.

3.11 The appellant is correct that in paragraph [0066] of D1 the purpose of determining whether a customer has left a restaurant is to alert the staff to a possible unpaid bill. The appellant goes on to argue that the skilled person would not find it obvious to use this method for the different purpose of triggering an automatic payment. This argument does not persuade the Board.

3.12 According to the Comvik approach the non-technical features of a claim may be incorporated into a goal to be achieved in a non-technical field. Subsequently, the approach invokes what might be described as the legal fiction that this goal, including the claimed non-technical features, would be presented to the skilled person, who would be charged with the task of technically implementing a solution which would achieve the stated goal. The question whether the skilled person would “arrive” at the non-technical features does not therefore arise, as these features have been made known to the skilled person, as part of the goal to be achieved. The relevant question for the assessment of inventive step is whether it would be obvious for the skilled person to implement a technical solution corresponding to the claimed subject-matter.

3.13 In the present case, automatic charging of the final amount to the customer when they leave the outlet represents the non-technical business aim (see above, point 3.6), and the relevant question is whether it would be obvious for the technically skilled person to implement this business aim according to the manner claimed. Asking whether it would be obvious to use the departure of a customer from a retail outlet to generate automatic charging of the customer amounts to asking whether the business aim is obvious. However, the business aim has, according to the above fiction, already been presented to the skilled person as part of the goal to be achieved, and hence this question does not arise in the Comvik approach and is irrelevant to the assessment of inventive step.

3.14 The appellant argued that payment according to paragraph [0045] of D1 involves several data transmission steps, whereas according to the claimed invention a single transmission of optimised data would reduce network usage, which was a technical effect.

3.15 Paragraph [0045] of D1 does indeed disclose a manual payment method involving several steps, which include the customer transmitting a request for the bill from a wireless device to a POS, the POS transmitting the bill to the customer, the customer reviewing the bill and, if satisfied, transmitting a payment confirmation and payment information to the POS, the customer possibly transmitting a request for assistance, and the transmission to the customer’s wireless device of a confirmation that the transaction has been completed.

These steps, and the resulting network usage, are the result of the payment method being manual, with the customer (and possibly the staff) being involved at every step. In a method where the amount is charged automatically, i.e. without any customer or staff involvement, all of the steps involving the customer and/or the staff would be eliminated, and a single transmission would be sufficient to initiate payment. In other words, any reduction in network usage which might be achieved by the method of claim 1, as compared to the method of paragraph [0045] of D1, would arise due to the claimed automatic charging.

3.16 Again it is pointed out that automatic charging is part of the non-technical business aim to be implemented by the skilled person, and since non-technical features have “no significance for the purpose of assessing inventive step” under the Comvik approach (see above, point 3.3), any analysis of the benefits or drawbacks of automatic charging is irrelevant. According to the legal fiction referred to above point [3.12], the requirement for automatic charging would simply be part of the specification given to the skilled person for technical implementation.

3.17 The appellant argues that the skilled person would be unable to implement automatic charging based on D1. The Board accepts that the payment schemes disclosed in D1 (e.g. paragraph [0045]) are manual, and that automatic charging is not disclosed. However, the technical implementation defined in claim 1 is at a very high level, involving, for example, receiving data and transmitting data, and it would be obvious to the skilled person that, to implement automatic payment, any steps disclosed in D1 involving transmission of data to or from the customer (or the staff) should be omitted, and that a single transmission containing only the information necessary to effect the transaction (payment account details, amount to be payed) would suffice.

3.18 If the appellant is arguing that the skilled person would be unable to implement automatic charging at a lower level (e.g. program modules, coding etc.) the Board’s view is that this would be within the capabilities of a skilled programmer. It is also noted that the present application does not contain any technical details of how the claimed steps are carried out other than at a high level, implying that the actual hardware and software measures required to achieve these steps would be readily understood by the skilled person. If this were not the case, then the absence of a detailed technical explanation in the application would mean that the invention was insufficiently disclosed (Article 83 EPC).

3.19 In the statement of grounds of appeal, the appellant argues that the method solves a technical problem in that infrastructure requirements can be reduced; for example, the need for point-of-sale (POS) terminals can be reduced or eliminated. The Board has been unable to identify any mention of this problem in the application, and it appears to be based on speculation. One could equally speculate that it is debatable whether any such savings would arise in practice, since it appears unlikely that a customer could be obliged to allow the location of their mobile device to be monitored (see, for example, D1, paragraph [0067]) or to pay a bill without having had the opportunity to check it, and presumably traditional infrastructure would have to be retained for those customers who refused to pay in this way.

3.20 In any event, the business person is always looking to reduce resource requirements, including staff and equipment, and envisaging a single payment arrangement which would automatically charge the customer at the end of their visit to the outlet is, at this level of abstraction, a non-technical idea which would be the province of the business person (who would delegate its implementation to the technically skilled person). For the reasons given above, the Board considers that, starting from D1, it would be obvious for the skilled person to arrive at the technical implementation of this business idea in the manner according to claim 1.

3.21 In the light of the above, the Board judges that the subject-matter of claim 1 of the main request does not involve an inventive step within the meaning of Articles 52(1) and 56 EPC.

Therefore, the Board decided that the subject-matter of claims does not involve an inventive step, and the application was refused.

More information

You can read the full decision here: T 0351/19 of June 23, 2022, of the Technical Board of Appeal 3.4.03.